P-Aminophenol Market Value: USD 485.6 Million in 2022 to USD 652.4 Million by 2029 at 4.3% CAGR

Global P-Aminophenol market was valued at USD 485.6 million in 2022 and is projected to reach USD 652.4 million by 2029, exhibiting a steady CAGR of 4.3% during the forecast period. This growth is driven primarily by increasing demand from the pharmaceutical and rubber industries, with significant contributions from emerging economies.

P-Aminophenol (PAP), an organic compound with the formula H2NC6H4OH, has evolved from a specialty chemical to an essential industrial intermediate. Its unique molecular structure, featuring both an amine and a hydroxyl group, enables diverse chemical reactions, making it invaluable for synthesizing numerous downstream products. Unlike many fine chemicals, PAP's production has achieved significant economies of scale, facilitating its integration into global supply chains for pharmaceuticals, dyes, and polymer stabilizers.

Get Full Report Here: https://www.24chemicalresearch.com/reports/229812/global-paminophenol-forecast-market-2023-2029-83

Market Dynamics:

The market's progression is defined by a series of powerful driving forces, notable constraints that industry participants are actively mitigating, and significant emerging opportunities across various applications.

Powerful Market Drivers Propelling Expansion

- Pharmaceutical Industry Demand Surge: The pharmaceutical sector stands as the cornerstone of PAP consumption, accounting for over 65% of global demand. This dominance is primarily due to its critical role as a key precursor in the synthesis of paracetamol (acetaminophen), one of the world's most widely used analgesics and antipyretics. Global production of paracetamol exceeds 150,000 tons annually, requiring a substantial and consistent supply of high-purity PAP. Furthermore, its application is expanding into other active pharmaceutical ingredients (APIs), including certain antimalarial and anticancer drugs, where its chemical properties enable precise molecular construction. The relentless growth of the global healthcare sector, particularly in aging populations and emerging markets, ensures sustained and growing demand for these essential medicines.

- Rubber and Polymer Industry Innovations: PAP serves as a vital building block for rubber antioxidants and antiozonants, such as p-phenylenediamine (PPD) derivatives. These additives are crucial for extending the service life of rubber products by 40-60% by inhibiting oxidative degradation caused by heat, oxygen, and ozone exposure. The global automotive industry, which consumes over 50% of the world's synthetic rubber for tires, hoses, and seals, is a primary driver. With the tire market alone valued at over $200 billion, the demand for high-performance antioxidants is robust. Recent innovations focus on developing next-generation, non-staining antioxidants derived from PAP for light-colored rubber goods, opening new market segments in consumer products and medical devices.

- Dyes and Pigments Manufacturing: The dyes industry leverages PAP's aromatic amine structure to produce azo dyes and sulfur dyes, which are renowned for their color fastness and vibrancy. These dyes are extensively used in textile, leather, and paper processing. The resurgence of the global textile industry, particularly in South and Southeast Asia, has revitalized this segment. PAP-based dyes are favored for their ability to create deep, consistent blacks and other dark shades that are resistant to washing and light exposure. The shift towards more environmentally friendly dyeing processes has also spurred R&D into new PAP-derived dye formulations with reduced environmental impact, aligning with stringent global regulations.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/229812/global-paminophenol-forecast-market-2023-2029-83

Significant Market Restraints Challenging Adoption

Despite its established applications, the market contends with several obstacles that temper its growth potential.

- Environmental and Regulatory Pressures: The production of PAP, particularly via the traditional iron powder reduction method, generates significant effluent containing iron sludge and other contaminants. Treating this wastewater to meet stringent environmental standards, such as EPA and REACH regulations, can increase production costs by 15-25%. Compliance requires advanced effluent treatment plants and continuous monitoring, which represents a substantial capital and operational expenditure, especially for smaller manufacturers. Regulatory bodies are increasingly scrutinizing aromatic amine compounds due to potential toxicity concerns, leading to complex and lengthy approval processes for new applications, sometimes extending beyond 24 months.

- Volatility in Raw Material Costs: PAP production is heavily dependent on key feedstock prices, particularly nitrobenzene and phenol, which are themselves derivatives of benzene. Benzene prices are notoriously volatile, influenced by crude oil fluctuations, petrochemical industry dynamics, and geopolitical factors. This price volatility, which can see 20-30% annual swings, creates significant uncertainty in PAP production economics. Manufacturers often struggle to pass these cost increases downstream immediately, squeezing profit margins and discouraging long-term investment in capacity expansion, particularly in regions with less integrated supply chains.

Critical Market Challenges Requiring Innovation

The industry faces a unique set of operational and technical hurdles that demand continuous innovation and strategic adaptation.

Manufacturing high-purity PAP, especially the pharmaceutical-grade material required for paracetamol synthesis, is a technically demanding process. Even minor impurities can render batches unsuitable for pharmaceutical use, leading to yield losses. Achieving consistent color index and particle size distribution for dyes and rubber applications also presents challenges. Batch-to-batch consistency remains a key differentiator among manufacturers, with top-tier producers achieving purity levels consistently above 99.8%, while others may experience variations that limit their market access to lower-value segments.

Furthermore, the industry must navigate a complex and sometimes fragmented global supply chain. Logistics for PAP require careful handling due to its classification as a potential skin and respiratory sensitizer. Transportation costs, particularly for international shipments complying with GHS labeling and SDS requirements, can add 5-10% to the final landed cost. Inventory management is also complicated by the compound's sensitivity to air and light, which can lead to discoloration and degradation if not stored properly, posing quality risks for end-users.

Vast Market Opportunities on the Horizon

- Green Synthesis Technologies: A major opportunity lies in the development and adoption of environmentally benign production methods. The hydrogenation reduction method, while more capital intensive, significantly reduces environmental impact compared to the iron powder process. Catalytic hydrogenation using novel catalysts can achieve yields exceeding 95% with minimal waste generation. Recent breakthroughs in continuous flow reactor technology for PAP synthesis promise further improvements in efficiency and safety, potentially reducing energy consumption by up to 30% and minimizing the footprint of production facilities. These advancements not only address environmental concerns but also offer economic benefits through reduced operating costs.

- Expansion into Niche Applications: Beyond its traditional uses, PAP is finding new roles in advanced material science. It is being explored as a monomer for designing novel polymers with enhanced thermal stability and mechanical properties. Research is ongoing into its use in photo-developing agents, corrosion inhibitors for specialty metals, and even in the synthesis of certain liquid crystal compounds for displays. The agrochemical sector is also investigating PAP derivatives as potential intermediates for new generation herbicides and pesticides, responding to the need for more effective and selective crop protection agents.

- Geographic Market Expansion: While mature in North America and Europe, significant growth potential exists in the Asia-Pacific region, particularly in India and China. These countries are not only major producers but also rapidly growing consumers of pharmaceuticals, rubber products, and dyes. Local manufacturing of paracetamol and tires is expanding dramatically to serve domestic and export markets. Furthermore, regions like Latin America and the Middle East present untapped opportunities as their industrial bases diversify and healthcare infrastructure improves, creating new demand centers for PAP and its downstream products.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented by production method into Hydrogenation Reduction Method and Iron Powder Reduction Method. The Hydrogenation Reduction Method is increasingly dominating the market, particularly for high-purity pharmaceutical-grade PAP. This method is favored because it produces a higher quality product with fewer impurities and is more environmentally sustainable, generating minimal solid waste compared to the iron powder process. The iron powder method, while historically significant and still used due to lower initial capital investment, is facing gradual phase-out in many regions due to environmental regulations.

By Application:

Application segments include Pharmaceutical Intermediate, Rubber Antioxidant, Dyes, and Others. The Pharmaceutical Intermediate segment is the clear market leader, consuming the lion's share of global PAP production. This is directly tied to the massive, steady demand for paracetamol worldwide. The Rubber Antioxidant segment holds a significant and stable share, driven by the global automotive and industrial rubber goods markets. The Dyes segment, while smaller, remains a consistent and high-value niche, particularly for specific azo black dyes.

By End-User Industry:

The end-user landscape is primarily composed of the Pharmaceutical, Rubber & Plastics, and Textile industries. The Pharmaceutical industry is the undisputed largest end-user, with its demand being relatively inelastic and driven by fundamental healthcare needs. The Rubber & Plastics industry is a critical secondary market, relying on PAP for product durability and longevity. The Textile industry, along with other smaller segments like Agrochemicals, rounds out the demand profile, each with specific quality and performance requirements.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/229812/global-paminophenol-forecast-market-2023-2029-83

Competitive Landscape:

The global P-Aminophenol market is moderately consolidated and features a mix of large, vertically integrated chemical conglomerates and specialized fine chemical manufacturers. The competitive environment is characterized by a strong focus on process technology, product quality consistency, and cost leadership. The top five players—including Anhui Bayi Chemical, Liaoning Shixing Pharmaceutical, and Mallinckrodt Pharmaceuticals—collectively account for approximately 55-60% of the global market share. Their leadership is reinforced by advanced manufacturing capabilities, extensive R&D focus on process improvement, and long-standing, reliable supply relationships with major end-users in the pharmaceutical sector.

List of Key P-Aminophenol Companies Profiled:

● Anhui Bayi Chemical (China)

● Liaoning Shixing Pharmaceutical (China)

● Farmson (India)

● Taixing Yangzi (China)

● Anqiu Lu'an Pharmaceutical (China)

● Mallinckrodt Pharmaceuticals (U.S.)

● Taizhou Nuercheng (China)

● Anhui Zhongxing Chemical (China)

● Meghmani Organics (India)

● Atabay (Turkey)

The prevailing competitive strategy hinges on securing long-term supply contracts with major pharmaceutical companies, continuous operational efficiency gains to maintain cost competitiveness, and strategic investments in cleaner production technologies to ensure regulatory compliance and sustainability.

Regional Analysis: A Global Footprint with Distinct Leaders

● Asia-Pacific: This region is the dominant force in the global PAP market, representing over 65% of both production and consumption. China and India are the epicenters of this dominance, fueled by their massive chemical manufacturing infrastructure, strong export-oriented pharmaceutical industries, and lower production costs. China, in particular, is the world's largest producer and consumer of paracetamol, creating immense captive demand for PAP.

● Europe and North America: Together, these mature markets account for approximately 25% of global demand. While their production share has declined relative to Asia, they remain critical consumers of high-purity PAP for their sophisticated pharmaceutical sectors. These regions are characterized by stringent quality standards and environmental regulations, which often makes production more costly, leading to a higher reliance on imports for standard grades while retaining specialty manufacturing.

● Rest of the World (Latin America, Middle East & Africa): These regions represent emerging but smaller markets, currently holding around 10% share. Growth here is driven by gradual industrialization, expanding pharmaceutical manufacturing capabilities, and development of local rubber and textile industries. However, these markets often face challenges related to infrastructure and regulatory frameworks, which can slow adoption and capacity development.

Get Full Report Here: https://www.24chemicalresearch.com/reports/229812/global-paminophenol-forecast-market-2023-2029-83

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/229812/global-paminophenol-forecast-market-2023-2029-83

Other related reports:

Mandarin Oil Market Size, Share,Global Outlook and Forecast 2023-2030

Iron Nickel Cobalt Alloy Market, Global Outlook and Forecast 2026-2033

Isobutyl Stearate Market, Global Outlook and Forecast 2026-2033

Enzymatic Plastic Degradation Market, Global Outlook and Forecast 2026-2033

Metal Putty Market, Global Outlook and Forecast 2025-2032

Silicon Dioxide for Dentistry Market, Global Outlook and Forecast 2025-2032

Tributyl Citrate Market, Global Outlook and Forecast 2024-2030

Resin Optical Lens Market, Global Outlook and Forecast 2025-2032

Post Consumer Film Recycling Market, Global Outlook and Forecast 2025-2032

Industrial Solvent Market, Global Outlook and Forecast 2026-2033

Contact us

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch

Kategorien

Mehr lesen

In-Depth Study on Executive Summary Pharmaceutical Packaging Market Size and Share CAGR Value The global pharmaceutical packaging size was valued at USD 118.43 billion in 2024 and is projected to reach USD 206.52 billion by 2032, with a CAGR of 7.20 % during the forecast period of 2025 to 2032. The world class Pharmaceutical Packaging Market business report presents with the...

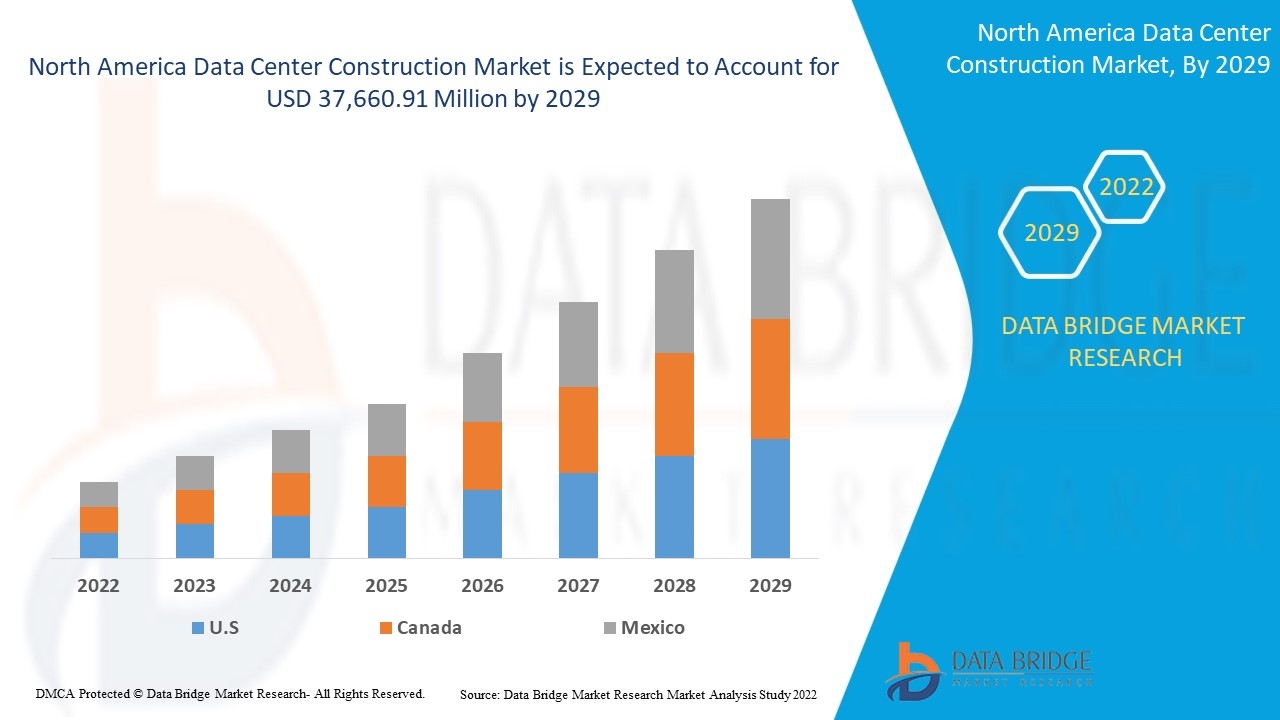

"Executive Summary: North America Data Center Construction Market Size and Share by Application & Industry CAGR Value North America Data Center Construction Market was valued at USD 15,988.24 million in 2021 and is expected to reach USD 37,660.91 million by 2029, registering a CAGR of 18.30% during the forecast period of 2022-2029. In the leading North America Data...

Executive Summary Bar and Prep Faucets Market : The bar and prep faucets market is expected to witness market growth at a rate of 8.41% in the forecast period of 2021 to 2028. Bar and Prep Faucets Market report is the best source that gives CAGR values with variations during the forecast period for the market. It provides CAGR (compound annual growth rate) values along...