Global Titanium Powder Market: Additive Manufacturing Propels Growth to USD 5.08 Billion by 2029

Global Titanium Powder market was valued at USD 4008.8 million in 2022 and is projected to reach USD 5081.4 million by 2029, exhibiting a CAGR of 3.4% during the forecast period. The influence of COVID-19 and the Russia-Ukraine War were considered while estimating market sizes.

Titanium powder, a finely divided form of the elemental metal, has transitioned from a niche material to a critical industrial feedstock. Renowned for its exceptional strength-to-weight ratio, unparalleled corrosion resistance, and high biocompatibility, titanium powder is the cornerstone of advanced manufacturing techniques like Additive Manufacturing (AM) and Metal Injection Molding (MIM). With purity levels ranging from 95% to an ultra-high 99.98%, this versatile material is indispensable across the aerospace, automotive, medical, and petrochemical sectors, enabling the production of complex, high-performance components that are often impossible to create with traditional methods.

Get Full Report Here: https://www.24chemicalresearch.com/reports/201052/titanium-powder-market-2023-2030-470

Market Dynamics:

The titanium powder market's evolution is driven by a potent combination of technological advancements and industrial demand, yet it must navigate significant production challenges and cost pressures to unlock its full potential.

Powerful Market Drivers Propelling Expansion

- Additive Manufacturing Revolutionizing Production: The single most significant driver is the explosive growth of Additive Manufacturing (3D Printing). The global AM market, projected to exceed $80 billion by 2030, is increasingly reliant on titanium powders for producing lightweight, complex aerospace components and custom medical implants. The ability to create lattice structures and topology-optimized parts can reduce component weight by 30-50%, a critical factor for fuel efficiency in the aviation sector, which consumes over 50% of all titanium produced. In the medical field, patient-specific implants, such as cranial plates and spinal fusion cages, are driving a segment growing at a CAGR well above the market average.

- Lightweighting Imperative in Automotive and Aerospace: The relentless pursuit of fuel efficiency and reduced emissions is a powerful force. The automotive industry's shift towards electric vehicles (EVs) intensifies the need for lightweighting to extend battery range. Titanium powder-based components, used in turbocharger wheels, connecting rods, and valve springs, offer a 40-50% weight reduction compared to steel alternatives. In aerospace, every 1 kg of weight reduction in an aircraft can lead to fuel savings of over $3,000 annually, making titanium powder a strategic material for both airframes and jet engines.

- Biomedical Implants and Healthcare Advancements: Titanium's biocompatibility makes it the material of choice for permanent implants. The aging global population is fuelling demand for orthopedic and dental implants. The global medical titanium market is expected to surpass $5 billion by 2027. Powder-based manufacturing allows for the creation of porous surfaces that promote osseointegration, where bone grows into the implant, significantly improving success rates. Furthermore, the rise of MIM for producing small, complex surgical instruments is creating a steady demand stream.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/201052/titanium-powder-market-2023-2030-470

Significant Market Restraints Challenging Adoption

Despite its superior properties, the market's growth is tempered by substantial economic and technical hurdles.

- High Cost of Production and Raw Material: The Kroll process, the primary method for producing titanium metal, is notoriously energy-intensive and costly, a cost that is passed on to the powder. Producing high-quality, spherical powder for AM via methods like Plasma Atomization or Plasma Rotating Electrode Process (PREP) adds another layer of expense. Consequently, titanium powder can be 10 to 20 times more expensive than commonplace metal powders like steel or aluminum, limiting its use to high-value applications where performance justifies the premium.

- Stringent Quality and Certification Requirements: In critical industries like aerospace and medical, the path to part certification is arduous. Powder consistency—including particle size distribution, flowability, and oxygen content—must be meticulously controlled. Variations in powder quality can lead to defective parts with compromised mechanical properties. The certification process for a new powder lot or a new AM process can take 12 to 24 months, acting as a significant barrier to rapid adoption and innovation.

Critical Market Challenges Requiring Innovation

The industry faces a dual challenge: scaling up production while driving down costs. Current atomization technologies have yield rates that can be as low as 60-70%, meaning a significant portion of the expensive raw material is lost. Furthermore, handling titanium powder requires an inert atmosphere (argon or vacuum) to prevent oxidation, which increases operational costs by 15-25% compared to handling less reactive metals. The supply chain is also susceptible to disruptions in the availability of titanium sponge, the primary raw material, whose production is concentrated in a few countries, leading to price volatility.

Moreover, the lack of standardized post-processing and quality control techniques across different AM platforms creates inconsistency. Issues like powder reuse and degradation after multiple printing cycles need to be fully understood and standardized to ensure part reliability and economic viability for end-users.

Vast Market Opportunities on the Horizon

- Next-Generation Production Technologies: Emerging processes like metalysis' FCC Cambridge process offer the potential to produce powder directly from titanium ore, bypassing the costly Kroll process. This could reduce production costs by up to 50%, potentially opening up new, cost-sensitive markets in automotive and consumer goods. Investments in these novel technologies exceeded $200 million in the last three years, signaling strong belief in their disruptive potential.

- Expansion into New Industrial Applications: Beyond aerospace and medical, titanium powder presents significant opportunities in the chemical processing industry (CPI). Its corrosion resistance makes it ideal for valves, pumps, and heat exchangers handling aggressive chemicals. The global corrosion-resistant alloy market, valued at over $20 billion, is a prime target. Additionally, the use of titanium MIM parts in high-end consumer electronics for durability and aesthetics is an emerging, high-growth niche.

- Recycling and Circular Economy Models: Developing efficient and certified methods for recycling unused titanium powder from AM processes is a major opportunity. Currently, 5-15% of powder in a build is not fused and can be reused. Establishing a robust recycling ecosystem could reduce material costs by 10-30% for end-users. Companies that develop reliable powder rejuvenation and requalification processes will create a significant competitive advantage and contribute to sustainable manufacturing practices.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into High Purity Titanium Powder (HPTP/CPTP) and Alloyed Titanium Powder (ATP). Alloyed Titanium Powder (ATP), particularly Ti-6Al-4V (Grade 5), dominates the market, accounting for over 60% of volume. This is because Ti-6Al-4V offers an optimal balance of strength, weight, and corrosion resistance, making it the workhorse alloy for aerospace and medical implants. High Purity Titanium Powder is essential for specific chemical applications where corrosion resistance is paramount and for some specialized electronic components.

By Application:

Application segments include the Aerospace Industry, Automobile Industry, Petrochemical Industry, and others. The Aerospace Industry is the largest and most established segment, driven by the relentless demand for lightweight, strong components for airframes and engines. However, the Medical application segment is experiencing the highest growth rate, fueled by the adoption of AM for custom implants and the expansion of MIM for surgical tools.

By End-User Industry:

The end-user landscape includes Aerospace, Automotive, Healthcare, Petrochemical, and others. The Aerospace industry accounts for the major revenue share, leveraging titanium's properties for critical, safety-dependent components. The Healthcare sector is the fastest-growing end-user, with its demand for biocompatible materials for implants and instruments. The Automotive industry is an emerging user, primarily in high-performance and luxury vehicles, with potential for growth as production costs decrease.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/201052/titanium-powder-market-2023-2030-470

Competitive Landscape:

The global Titanium Powder market is semi-consolidated and characterized by the dominance of a few key players with advanced technological capabilities. The top five manufacturers—ATI (US), Cristal (Saudi Arabia), OSAKA Titanium (Japan), Fengxiang Titanium (China), and Reading Alloys (US)—collectively command approximately 65% of the global market share. Their leadership is cemented by vertically integrated operations, control over titanium sponge production, extensive intellectual property portfolios related to powder production, and long-standing relationships with major aerospace and medical OEMs.

List of Key Titanium Powder Companies Profiled:

● ATI (U.S.)

● Cristal (Saudi Arabia)

● OSAKA Titanium (Japan)

● Fengxiang Titanium (China)

● ADMA Products (U.S.)

● Reading Alloys (U.S.)

● MTCO (U.S.)

● TLS Technik (Germany)

● Global Titanium (U.S.)

● GfE (Germany)

● AP&C (Canada, a GE Additive company)

● Puris (U.S.)

● Toho Titanium (Japan)

● Metalysis (U.K.)

● Praxair S.T. Tech (U.S.)

The competitive strategy is heavily focused on Research & Development to improve powder quality, develop new alloys, and reduce production costs. Furthermore, forming strategic partnerships with end-users, particularly in the AM sector, to co-develop qualified processes and secure long-term supply agreements is a critical tactic for market leadership.

Regional Analysis: A Global Footprint with Distinct Leaders

● North America: Is the dominant force, holding a 60% share of the global market. This leadership is driven by the presence of a massive aerospace and defense industry (Boeing, Lockheed Martin, GE Aviation), a world-leading medical device sector, and significant investments in additive manufacturing R&D. The United States is the primary engine of growth.

● Europe & Asia-Pacific: Europe holds a significant share, supported by a strong aerospace sector (Airbus, Safran) and advanced manufacturing base. The Asia-Pacific region, particularly Japan and China, is a powerhouse in both production and consumption. Japan is a technological leader in titanium sponge and powder production, while China's massive industrial base and growing aerospace and medical sectors are driving rapid demand growth.

● Rest of the World (South America, MEA): These regions represent emerging markets with growing potential. Growth is primarily driven by increasing industrialization, investments in energy and chemical infrastructure, and the gradual adoption of advanced manufacturing technologies.

Get Full Report Here: https://www.24chemicalresearch.com/reports/201052/titanium-powder-market-2023-2030-470

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/201052/titanium-powder-market-2023-2030-470

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Catégories

Lire la suite

Market Trends Shaping Executive Summary Golf Shoes Market Size and Share The global golf shoes market size was valued at USD 9.23 billion in 2024 and is expected to reach USD 11.79 billion by 2032, at a CAGR of 3.10% during the forecast period. The Golf Shoes Market report puts light on the change in the market which is taking place due to the...

A popular post on Reddit captures the issue in a meme. The top text on the meme reads "Keep one adventurer alive," referencing the Diablo 4 Items goal for mastering the encounter. The bottom text reads, "Aaaand they're gone," since they die so quickly. A second Reddit posts on the subject details a player's frustrations in more detail. They say the encounter is a joke, that the adventurers die...

Executive Summary Solar Panel Cleaning Market : Global Solar Panel Cleaning Market was valued at USD 591.00 million in 2021 and is expected to reach USD 1,505.63 million by 2029, registering a CAGR of 12.40% during the forecast period of 2022-2029. Solar Panel Cleaning Market report has been designed by keeping in mind the customer requirements which assist them in increasing their...

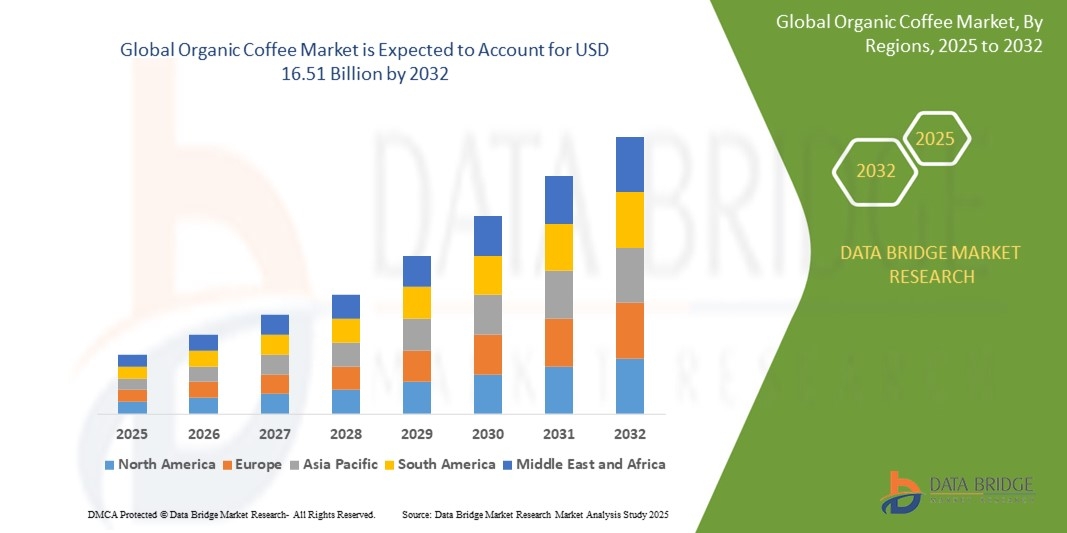

Introduction The Organic Coffee Market represents the global industry focused on the cultivation, processing, distribution, and sale of coffee produced without synthetic fertilizers, pesticides, or genetically modified organisms. Organic coffee follows strict agricultural and certification standards that emphasize soil health, biodiversity, and environmentally responsible farming...

Executive Summary Middle East and Africa Cartoning Machines Market : Data Bridge Market Research analyses that the Middle East and Africa cartoning machines market which was USD 36.20 million in 2022, is expected to reach USD 54.64 million by 2030, growing at a CAGR of 5.3% during the forecast period of 2023 to 2030. Today’s cut-throat era calls for businesses to be...