Oil and Gas Accumulator Market: Growth, Trends, and Future Outlook

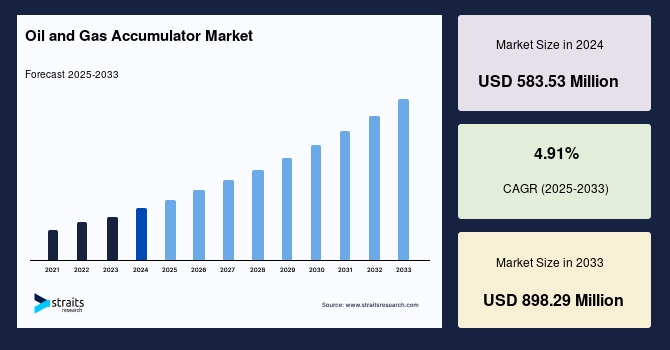

The global oil and gas accumulator market size was valued at USD 583.53 million in 2024 and is projected to reach from USD 612.18 million in 2025 to USD 898.29 million by 2033, growing at a CAGR of 4.91% during the forecast period (2025-2033).

Overview of Oil and Gas Accumulators

Oil and gas accumulators are specialized hydraulic devices that store potential energy to provide instantaneous energy release when required. They play vital roles in shock and pulsation dampening, leakage compensation, noise reduction, thermal expansion management, and energy conservation in oilfield operations. The accumulators support a variety of applications, including drilling rigs, blowout preventer (BOP) systems, offshore platforms, and hydraulic power units.

Three main types dominate the market: bladder, diaphragm, and piston accumulators. Each type has unique characteristics tailored to specific operational demands in temperature tolerance, durability, and fluid handling capabilities.

Market Dynamics and Growth Drivers

The oil and gas accumulator market growth is fueled primarily by ongoing exploration and production activities. Increasing drilling of new wells, especially in emerging fields, has pushed the need for advanced accumulator systems to enhance safety and operational efficiency. Blowout preventers, which rely heavily on accumulators, are crucial in avoiding catastrophic drilling incidents, thus driving demand.

Digital innovation is another key growth driver. Leading oil and gas companies are adopting artificial intelligence, machine learning, and data analytics to improve well delivery, maintenance, and production optimization. These technologies help integrate accumulators into smarter hydraulic control systems, boosting their performance and reliability.

The market’s regional growth is led by North America due to its active shale gas exploration, rising crude oil output, and favorable government policies supporting upstream investments. Onshore applications dominate as they require lower investment than offshore developments but account for a growing number of new wells needing accumulator installations.

Asia-Pacific is poised for rapid expansion, attributed to increasing energy demand and intensified drilling activities in countries like China and India. The Middle East is expected to grow moderately, backed by its vast energy reserves and ongoing crude oil exploration projects.

Segmentation Insights

By Type

-

Bladder Accumulators: Leading the market share, bladder accumulators are favored for their high durability, efficiency, and ability to support blowout preventer systems globally. They find use in fluid volume compensation, hydraulic power units, wind energy, and other industrial settings.

-

Piston Accumulators: Known for their customization options and robust performance under extreme temperatures, piston accumulators see rising adoption in oil and gas and other industries such as marine and aerospace.

-

Diaphragm Accumulators: These are valued for fluid storage and low-volume pulsation dampening in mobile and off-road markets, with flexibility in handling different liquid-to-gas ratios and orientations.

By Application

-

Blowout Preventer Systems: Representing the highest growth segment, accumulators in BOPs are essential for safety during drilling operations, especially in onshore and offshore fields.

-

Onshore and Offshore Rigs: Offshore accumulator demand is significant but grows slower compared to onshore owing to higher investment costs offshore. Onshore drilling expansion, particularly in newly developed fields, requires extensive accumulator deployment to ensure safety and functionality of drilling equipment.

Challenges and Constraints

Despite its promising outlook, the oil and gas accumulator market faces several hurdles. High initial costs and the bulky, heavy nature of accumulators limit mobile transportation and deployment flexibility. Additionally, environmental risks from drilling-associated oil spills have led to stringent regulations by bodies such as the U.S. Environmental Protection Agency (EPA). These environmental mandates could constrain expansion unless industry players innovate towards safer, more efficient accumulator designs.

Competitive Landscape

The market is moderately fragmented with a few dominant players advancing through technology innovations and strategic partnerships. Leading companies focusing on hydraulic systems for oil and gas include Eaton Corporation PLC, Parker-Hannifin Corporation, Hydac, Freudenberg Group, and Roth Industries. These companies are pushing forward research and development in accumulator technology, addressing challenges of durability, energy efficiency, and integration with digital monitoring systems.

Future Outlook

The oil and gas accumulator market is set for steady growth through 2033, aligning with the broader upstream sector’s development and digital transformation. Strategic investments in shale gas and natural gas production, coupled with increasing safety regulations, will stimulate demand for accumulators globally.

With advancements in digital technologies and hydraulic control systems, accumulator efficiency and functionality will continue to improve, driving market evolution. Regions such as North America and Asia-Pacific will continue to be focal points, while emerging energy markets may present new opportunities.

In conclusion, oil and gas accumulators remain critical components underpinning safety and operational effectiveness in the energy sector. Continued innovation, regulatory compliance, and expanding upstream activities will ensure the market’s sustained growth in the years ahead.

Категории

Больше

"Executive Summary Thermoformed Shallow Trays Market : An international Thermoformed Shallow Trays Market research report is an absolute overview of the market that spans various aspects such as product definition, customary vendor landscape, and market segmentation based on various parameters such as type of product, its components, type of management and geography....

When intermittent power outages plague remote installations, an outdoor electrical distribution panel may be at the heart of the problem. Exposure to moisture, dust and temperature extremes can degrade components and undermine reliable delivery of current. Before blaming upstream supply or expensive equipment, technicians should examine the enclosure carefully. Identifying common fault sources...

The Multimedia Chipsets Market is experiencing significant growth, driven by the rapid evolution of consumer electronics, increased demand for high-resolution media content, and the expansion of connected devices. Valued at US$ 29,920.32 million in 2024, the market is projected to grow at a CAGR of 6.20% between 2025 and 2032. Multimedia chipsets, which serve as the backbone of audio, video,...

The global Attendant Console market leads the nation's so-called 'renaissance', such that each industrial segment is endowed with well-efficient and networked solutions. IT infrastructure forms a necessity, ranging from cloud storage to cybersecurity. Based on market performance during 2025-2032, the sector experiences a CAGR of 10.2%, whereas valuation continues to provide proof of the...